Retirement income after age 60 is often misunderstood. Many people assume it works like a paycheck replacement—stop working, start withdrawing, and maintain the same financial rhythm. In reality, retirement income behaves very differently from employment income, and misunderstanding those differences is one of the most common causes of financial stress later in life.

This article explains how retirement income actually works, what changes after age 60, and why planning for income stability matters more than chasing returns.

Retirement Income Is a System, Not a Single Source

Before retirement, income is usually straightforward: wages or salary arrive regularly, taxes are withheld, and spending follows a predictable cycle. After age 60, income typically comes from multiple sources, each with its own rules, timing, and risks.

Common retirement income sources include:

- Social Security benefits

- Pensions (if applicable)

- Investment portfolio withdrawals

- Dividends and interest

- Required Minimum Distributions (later in retirement)

- Part-time or consulting income

The key shift is that no single source replaces a paycheck. Retirement income works as a system where timing, coordination, and sustainability matter more than raw totals.

Guaranteed Income vs. Variable Income

One of the most important distinctions in retirement income planning is the difference between guaranteed and variableincome.

Guaranteed Income

This includes sources that are predictable and largely immune to market fluctuations:

- Social Security

- Defined benefit pensions

- Certain annuities

Guaranteed income provides stability. It covers essential expenses and reduces dependence on market performance.

Variable Income

This includes:

- Portfolio withdrawals

- Dividends

- Interest income

- Capital gains

Variable income fluctuates with markets, interest rates, and economic conditions. It requires active management and discipline, especially during market downturns.

Most retirement plans blend both types, but problems arise when retirees overestimate the reliability of variable incomeor underestimate how long retirement may last.

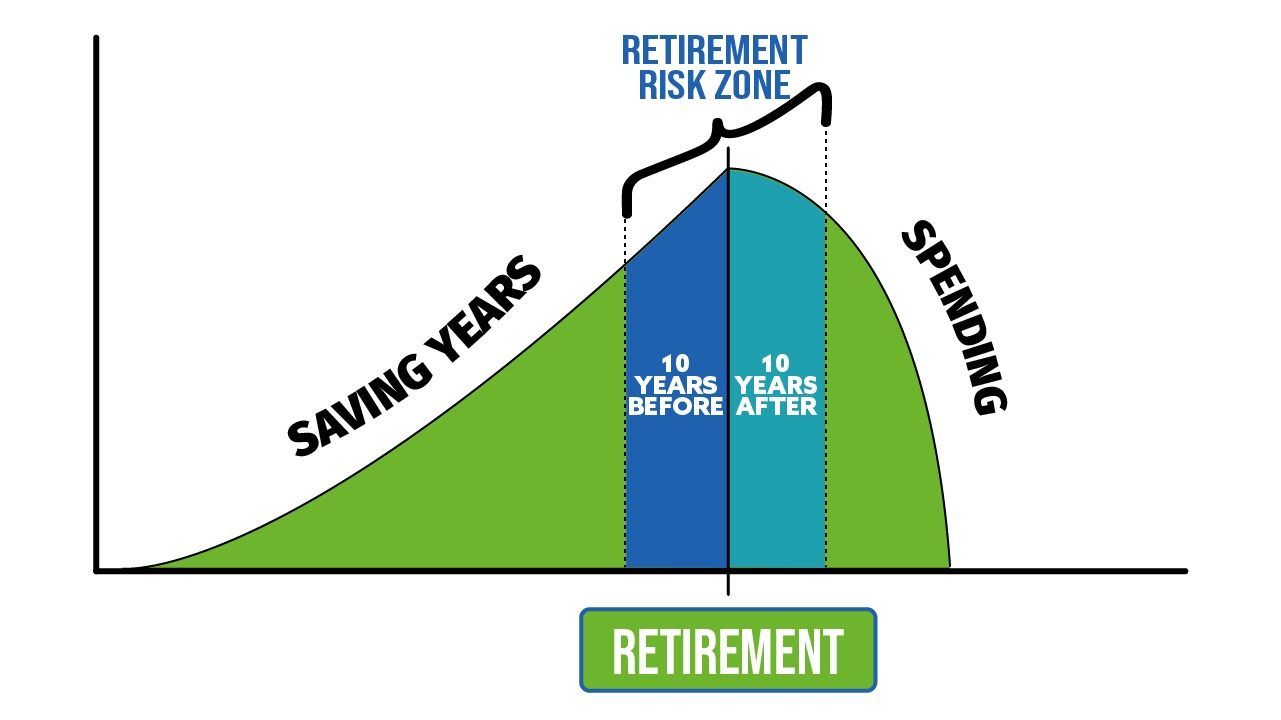

The Timing of Income Matters More Than the Amount

Two retirees can have identical net worths and very different outcomes. The difference is often when income is taken, not how much money exists on paper.

Key timing factors include:

- When Social Security benefits are claimed

- Sequence of withdrawals from taxable, tax-deferred, and tax-free accounts

- Market conditions during early retirement years

- Required Minimum Distributions beginning later in life

Early mistakes compound. Large withdrawals during market downturns can permanently reduce a portfolio’s ability to recover, even if markets eventually rebound.

Retirement Income Is Not Linear

Employment income tends to be steady and predictable. Retirement income is not.

Spending patterns often change over time:

- Early retirement may involve higher discretionary spending

- Mid-retirement often stabilizes

- Later retirement may see increased healthcare costs

At the same time, income sources may shift:

- Social Security may increase modestly with inflation

- Portfolio withdrawals may need adjustment

- Required distributions can force higher taxable income later

Successful retirement income planning accounts for these phases rather than assuming a flat, unchanging draw.

Taxes Play a Larger Role Than Expected

Many retirees are surprised to learn that their tax situation can become more complex after leaving the workforce.

Factors that affect retirement taxation include:

- Social Security benefit taxation

- Withdrawals from traditional retirement accounts

- Capital gains recognition

- Medicare income-related premium adjustments

Poor coordination between income sources can lead to unnecessary taxes, even when overall spending remains modest.

Understanding how income flows through the tax system is a core component of sustainable retirement income—not an afterthought.

Longevity Is the Hidden Variable

One of the greatest risks in retirement is not market volatility—it is outliving income.

At age 60, it is entirely reasonable to plan for a 30-year retirement. Income decisions made early must support decades of spending, inflation, and uncertainty.

This reality shifts the goal from:

“How much can I take this year?”

to:

“How do I make income last for the rest of my life?”

That change in mindset is often the difference between confidence and chronic anxiety.

Why Simplicity Improves Outcomes

Complex retirement income strategies often fail not because they are mathematically flawed, but because they are difficult to maintain.

Plans that work best tend to:

- Prioritize clarity over optimization

- Reduce reliance on perfect market conditions

- Emphasize repeatable processes

- Adjust gradually rather than react emotionally

A retirement income plan that is understood and followed consistently is usually superior to a complex plan that looks better on paper but is abandoned under stress.

The Big Picture

After age 60, retirement income becomes a dynamic management process, not a static calculation. It requires:

- Coordinating multiple income sources

- Balancing stability and flexibility

- Managing taxes thoughtfully

- Adjusting over time as life changes

The objective is not maximizing income in any single year. It is creating a sustainable, understandable system that supports your lifestyle without exposing you to unnecessary risk.

Understanding how retirement income really works is the foundation for every other decision that follows.

This article is educational in nature and intended to support informed decision-making. Individual circumstances vary, and professional guidance may be appropriate.

Leave a Reply