When investors talk about building wealth, the conversation usually begins with growth. Increasing account values, accumulating assets, and maximizing long-term returns are common priorities during working years.

As retirement approaches, however, the focus often shifts. The central question becomes less about how large a portfolio appears on paper and more about how reliably it can support ongoing expenses. This is where understanding income versus growth becomes especially important.

Recognizing the difference between these two approaches—and when each one matters most—can help reduce financial stress and improve long-term retirement confidence.

What Does Investing for Growth Mean?

Investing for growth generally focuses on increasing the value of a portfolio over time. The emphasis is on assets expected to appreciate, even if they produce little or no current income.

Common characteristics of growth investing include:

- A primary focus on capital appreciation

- Greater exposure to market volatility

- Returns that often depend on selling assets in the future

During accumulation years, growth investing can be effective because time and continued contributions help smooth out market fluctuations. Temporary declines may feel uncomfortable, but they are often manageable while employment income continues.

What Does Investing for Income Mean?

Investing for income prioritizes ongoing cash flow rather than portfolio value alone. The objective is to generate regular income that can help cover living expenses without requiring frequent asset sales.

Income-oriented strategies typically emphasize:

- More predictable cash distributions

- Reduced reliance on market timing

- Greater attention to sustainability and risk control

The concept of investing for income is commonly defined as focusing on generating regular income from investments rather than relying solely on price appreciation.

For retirees, this approach can align investments more closely with real-world spending needs.

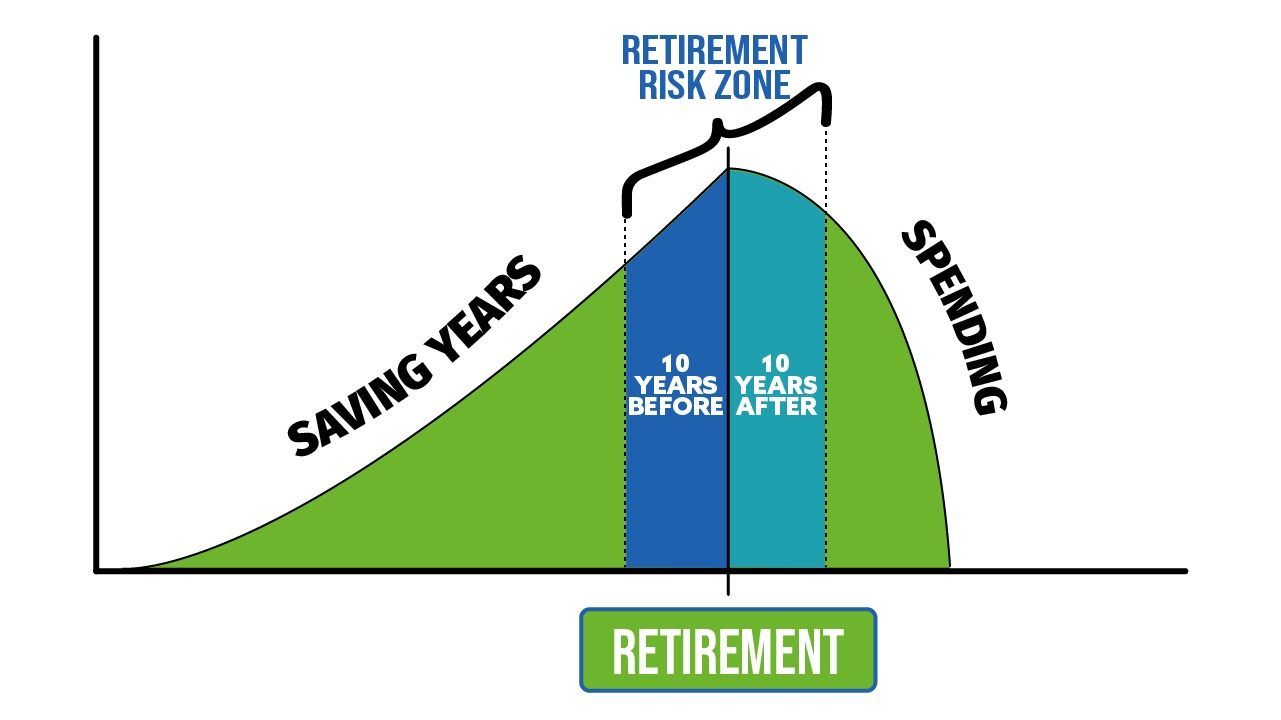

Why the Difference Matters More in Retirement

The distinction between income versus growth becomes more meaningful once withdrawals begin.

In retirement:

- Market declines may force investors to sell assets at unfavorable prices

- Early losses can have lasting consequences, often described as sequence-of-returns risk

- Volatility can directly affect income stability and confidence

This is why income investing vs growth investing in retirement is not an abstract discussion. The structure of a portfolio influences how retirees experience market downturns and whether income needs can be met without disruption.

These dynamics are explored further in What Is Sequence-of-Returns Risk and Why It Matters in Retirement.

Growth and Income Are Not Opposites

Growth and income are not mutually exclusive. Most portfolios contain elements of both. The key difference lies in which objective takes priority.

- Growth-focused portfolios emphasize future value

- Income-focused portfolios emphasize present cash flow

As investors age, priorities often evolve. Growth may still play a role, but income typically becomes more central to maintaining financial stability.

How Income Investing Changes the Retirement Experience

Income-oriented portfolios can change how retirees experience market volatility. Instead of reacting to daily price movements, attention shifts to whether income remains reliable and sufficient.

For many retirees, guaranteed income sources such as Social Security retirement benefits form the foundation of retirement cash flow, with portfolio income providing additional support:

https://www.ssa.gov/benefits/retirement/

Understanding how retirement income actually works after age 60—including the interaction between Social Security, portfolio income, and withdrawals—can make market downturns easier to navigate.

This shift in perspective may:

- Reduce emotional stress during volatile markets

- Lower the need for reactive decision-making

- Improve confidence in long-term planning

Choosing the Right Emphasis at the Right Time

There is no single strategy that fits every investor. The appropriate balance between growth and income depends on factors such as:

- Retirement timing and income flexibility

- Spending needs and lifestyle expectations

- Risk tolerance and emotional comfort

For many investors, income investing becomes more important as you get older, not because growth stops mattering, but because consistency and predictability become more valuable.

How This Fits Into Simple Income Investing

Simple Income Investing is a conservative, education-first framework designed to help retirees understand how income, risk, and portfolio structure interact in real-world retirement scenarios.

Rather than emphasizing market forecasts or short-term performance, the approach prioritizes:

- Reliable cash flow

- Awareness of retirement-specific risks

- Practical decision-making as income needs increase

If you are new to these concepts or want a structured way to navigate them, begin here:

Start Here: How to Use Simple Income Investing as You Approach Retirement

Final Thoughts

The difference between investing for growth and investing for income reflects a broader shift in priorities as retirement approaches.

Understanding income versus growth allows investors to make more intentional choices, particularly when dependable income becomes more important than maximizing upside.

As retirement nears, clarity often matters more than complexity. A strategy that emphasizes sustainable income may not always look impressive during strong markets, but it can provide something far more valuable over time: confidence.upports reliable income may not always look impressive on paper, but it can provide something far more valuable: confidence.

Leave a Reply