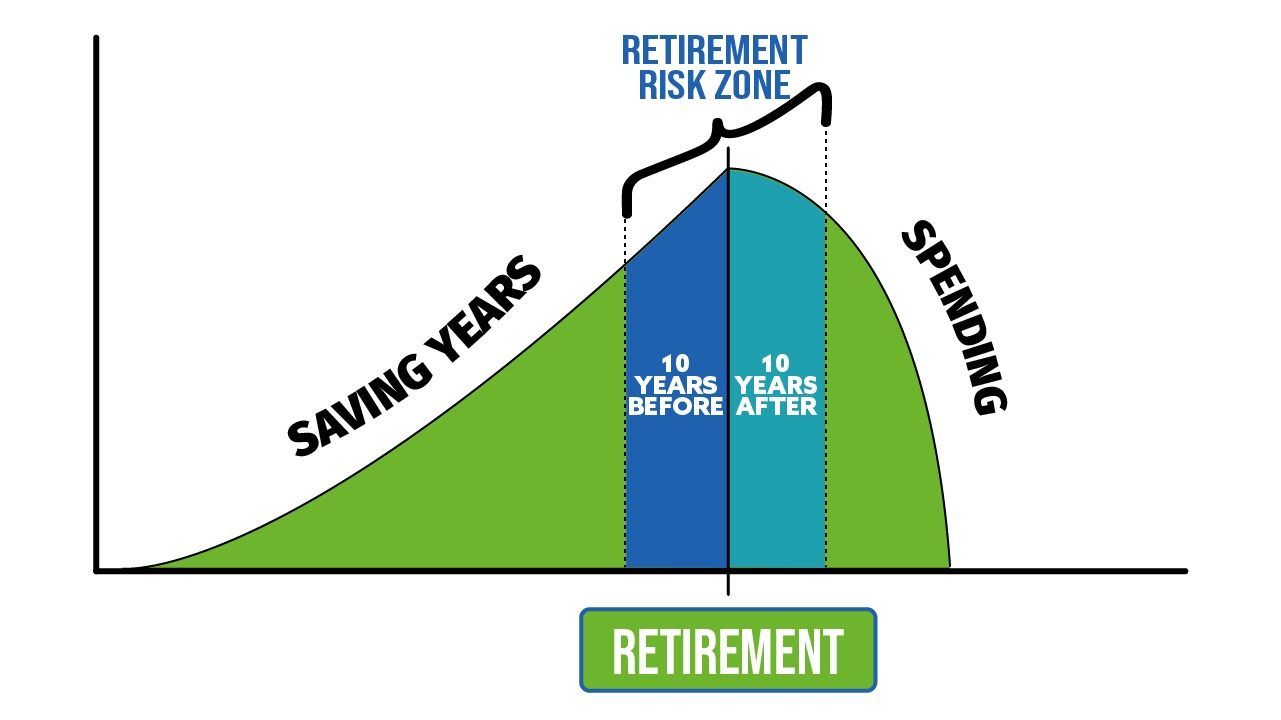

For many people, retirement introduces a new kind of financial uncertainty—not because they lack money, but because they lose visibility. Paychecks stop, income arrives from multiple sources, and expenses no longer follow a predictable rhythm. Even retirees who planned carefully often describe the same feeling: “I think we’re fine, but I don’t feel as confident as I expected.”

That uncertainty is almost always a cash flow issue, not a wealth issue.

The good news is that effective retirement cash flow tracking does not require complex spreadsheets or constant monitoring. It requires a simple system that reflects how retirement income actually behaves.

Why Cash Flow Matters More Than Net Worth in Retirement

Before retirement, net worth is often used as a scorecard. After retirement, it becomes far less useful on its own.

You cannot spend net worth.

You spend income.

A Real-Life Example

Consider two retirees, both with $1 million saved.

- Retiree A has steady Social Security income and modest, predictable expenses.

- Retiree B relies heavily on portfolio withdrawals that vary with market conditions.

Even with the same net worth, Retiree A typically experiences less stress and more confidence, simply because income is visible and reliable.

Cash flow answers the question retirees actually care about:

“Can I comfortably support my lifestyle without worrying every month?”

The Core Shift: From Budgeting to Monitoring

Traditional budgeting assumes:

- A regular paycheck

- Predictable monthly income

- Tight expense categories

Retirement rarely works that way.

Instead of rigid budgeting, retirees benefit from cash flow monitoring—a system focused on awareness and trends rather than control and precision.

Case Study: Why Simpler Works Better

A recently retired couple tried to track 25 spending categories in a spreadsheet. After three months, they stopped updating it. The system was technically accurate—but emotionally exhausting.

They replaced it with a monthly income-versus-expense summary. The result: better consistency, clearer insight, and significantly less anxiety.

Step 1: Identify Your True Income Sources

Start with income you can reasonably rely on, not optimistic projections.

Typical sources include:

- Social Security (net of Medicare premiums)

- Pension payments

- Scheduled portfolio withdrawals

- Dividends and interest

- Part-time income (if applicable)

Avoid including:

- Market gains that have not been realized

- One-time windfalls

- Withdrawals you “might” take later

This approach keeps your cash flow picture realistic and grounded.

Step 2: Separate Fixed and Flexible Expenses

Instead of tracking dozens of categories, divide expenses into just two groups.

Fixed Expenses

- Housing

- Utilities

- Insurance

- Healthcare premiums

- Basic transportation

Flexible Expenses

- Travel

- Dining out

- Entertainment

- Gifts

- Hobbies

This distinction matters because flexibility equals resilience. Knowing which expenses can be adjusted provides reassurance during uncertain periods.

Step 3: Track Monthly Net Cash Flow (Not Every Transaction)

You do not need to track every expense in real time.

Once per month, record:

- Total income received

- Total expenses paid

- Net surplus or shortfall

This high-level snapshot is enough to reveal:

- Whether withdrawals are increasing

- If spending patterns are changing

- Whether adjustments are needed

Clarity improves confidence. Precision beyond this point rarely improves outcomes.

Step 4: Use Rolling Averages to Reduce Stress

Retirement spending is uneven by nature.

A single expensive month—travel, home repairs, medical costs—can create unnecessary worry if viewed in isolation. Reviewing cash flow over three-month periods provides better context and discourages emotional overreactions.

Step 5: Maintain a Cash Buffer

A cash buffer covering three to six months of core expenses acts as an emotional and financial stabilizer.

It:

- Smooths income timing gaps

- Reduces the need for reactive investment decisions

- Helps retirees stay disciplined during market volatility

Many retirees report that simply knowing the buffer exists improves sleep and decision-making.

The Emotional Side of Cash Flow Decisions

Financial decisions in retirement are rarely just mathematical. They are deeply emotional.

Uncertainty can lead to:

- Overspending to “enjoy life while we can”

- Underspending out of fear

- Constant second-guessing

A clear cash flow system reduces emotional noise. When income and expenses are visible, decisions feel calmer and more intentional.

Frequently Asked Questions

Do I need a detailed budget in retirement?

No. Most retirees do better with monitoring rather than strict budgeting.

How often should I review cash flow?

Monthly tracking with quarterly trend reviews is sufficient for most people.

What if one month looks bad?

Look for patterns, not single data points. One month rarely tells the full story.

Should I track investments daily?

Daily monitoring increases stress without improving outcomes. Monthly or quarterly reviews are usually adequate.

Getting Started: One Simple Action

If you do nothing else this week, do this:

Write down last month’s total income, total expenses, and the difference.

That single step creates awareness—and awareness is the foundation of confident retirement income management.

Final Thought

Tracking retirement cash flow does not require complexity. It requires:

- Realistic income assumptions

- Clear expense categories

- Periodic review

- Emotional discipline

When cash flow is visible and understandable, retirement decisions become steadier, more deliberate, and far less stressful.

This article is educational in nature and intended to support informed financial awareness. Individual circumstances vary, and professional guidance may be appropriate.

Leave a Reply